Consumers, small businesses hurting from inflation: Alfredo Ortiz

Job Creators Network President Alfredo Ortiz reacts to cooling inflation rates but high ‘overall’ inflation, saying domestic oil drilling and less domestic spending could help the ‘overall economy.’

The Consumer Financial Protection Bureau was conceived in the fallout of the 2008 financial crisis. The intent of the agency’s formation, authorized by the 2010 Dodd–Frank Wall Street Reform and Consumer Protection Act, is noble and self-evident: to protect the financial health of American consumers.

However, recent concerning incidents have revealed that the overzealous runaway agency is on a collision course with American consumer interests: from questionable personnel choices to data breaches and absent consumer notifications, it is evident that the CFPB needs a "Casey Jones" to halt derailment.

Originally headed by Richard Cordray, President Barack Obama called a recess appointment to install the inaugural director, a maneuver that was later unanimously ruled unconstitutional in NLRB v. Noel Canning. Fast-forward to 2016 and David Silberman takes charge. Silberman’s long and conflicted history of unabashedly attacking financial products is hardly the position of an impartial arbiter and still raises doubts about his objectivity and ability to provide an unbiased assessment. His efforts plague the financial services sector even today through his involvement with the Center for Responsible Lending.

Sen. Elizabeth Warren proposed the Consumer Financial Protection Bureau when she was still a Harvard professor. (AP Photo/Alex Brandon)

But this year, the CFPB reached breakneck speeds with its nonbank disclosure rule. The rule mandates that certain nonbank entities report public enforcement orders to a designated registry. However, it risks damaging public trust in emerging financial institutions, disrupts state and local oversight processes, and imposes burdensome compliance requirements on businesses. A coalition of organizations urged the CFPB to reconsider this rule, emphasizing the need for a balanced approach that considers the impact on all stakeholders.

I’ve never seen anything as clear as this: the CFPB’s piercing whistle is sounding as they round the bend, careening into the financial sector.

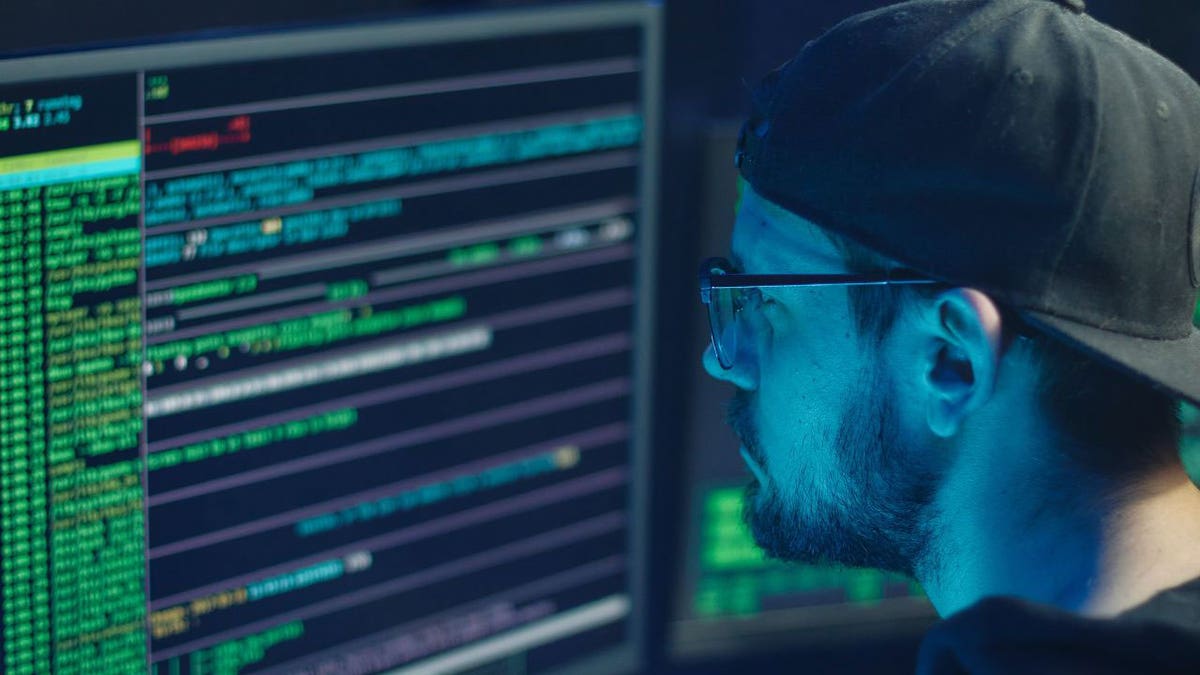

Like clockwork, a data breach occurred at the CFPB, where an employee forwarded the personal information of over 250,000 consumers to that employee’s personal email account. The delayed notification of affected consumers, occurring nearly two months after the breach, raises serious questions about the CFPB's ability to handle and safeguard sensitive information.

As of April, the victims of the data breach had still not been notified that their personal information had been compromised. (CyberGuy.com)

This incident underscores the need for stricter data privacy measures and immediate actions to mitigate the potential harm caused by such breaches. The worst part? As of April, the victims of the data breach had still not been notified that their personal information had been compromised.

CONSUMER FINANCE BUREAU ‘OUT OF CONTROL’ UNDER BIDEN'S DIRECTOR, CRITICS SAY

Yes, you read that right. The same organization that just last year published a circular declaring that "financial companies may violate federal consumer financial protection law when they fail to safeguard consumer data" has quite literally done exactly that. "Do as I say, not as I do," or so the saying goes.

If the CFPB is watching financial institutions for bad behavior, who’s watching the CFPB?

Sen, Tim Scott has announced his intentions to target the new CFPB data collection rules. (Mel Musto/Bloomberg via Getty Images)

In a span of less than three weeks, the damage had been done: the CFPB was instituting demands for increased data collection while simultaneously breaching the public trust with their inept management of consumer data. Republican lawmakers have rightfully requested briefings on the data breach, ensuring that bad actors are held accountable. Presidential hopeful Sen. Tim Scott, R-S.C., announced his intentions to target the new CFPB data collection rules. Scott’s spokesman said, "If the CFPB cannot protect the data it has now, why should Americans trust it with more data?"

At this point, is there any reason to attempt salvaging the beleaguered bureau?

CLICK HERE TO SIGN UP FOR OUR OPINION NEWSLETTER

Once established with the goal of protecting consumers and promoting fair financial practices, the CFPB has exposed a rotten core. It’s clear from the narrative surrounding the agency’s inception coupled with the inability of the bureau to protect Americans from its own employees that it’s doing more harm than good.

With a track record like that, maybe it’s time to consider hitting the brakes before the runaway train causes any more damage to American consumer confidence.

Best of Opinion

Get the recap of top opinion commentary and original content throughout the week.

By entering your email and clicking the Subscribe button, you agree to the Fox News Privacy Policy and Terms of Use, and agree to receive content and promotional communications from Fox News. You understand that you can opt-out at any time.